Orange Oil CP

Citrus sinensis

Harvest: July - December

Brazil’s total orange production for the new 2020/2021 crop, starting in July, is expected to be 22% lower than the current crop ending in June 2020. It is estimated at around 370 million boxes (15.1 million MT) compared with the final forecast for the current season of 475 million boxes (19.4 million MT) for all production regions in Brazil. This estimated decrease is mainly a result of alternate bearing (discussed below) and weather-related problems such as warmer than usual temperatures and below average rainfall after the first two blossoms and fruit set in São Paulo State, the dominant growing area.

The latest Fundecitrus report released in early May confirms a reduction of 25.6% for the 2020/2021 crop to 287.76 compared to the previous crop of 386.79 million boxes. This forecast is for the São Paulo and West-Southwest Minas Gerais citrus belt, which accounts for approximately three-quarters of Brazilian production. The expected 287.76 million boxes include:

- 45.53 million boxes of Hamlin, Westin and Rubi

- 13.05 million boxes of Valencia Americana, Seleta and Pineapple

- 87.04 million boxes of Pera Rio

- 106.16 million boxes of Valencia and Valencia Folha Murcha

- 35.98 million boxes of Natal

Some 85% of production will come from the first and second blooms, while 12% and 8%, respectively, will come from the third and fourth blooms.

Apart from the adverse weather conditions affecting the crop, this season is also experiencing a significant reduction in the number of fruits per trees compared to that in the previous crop. This is due to the large production in the last season which increased the consumption of nutrient reserves in plants. As a result of this phenomenon, known as alternate bearing, average yield is estimated to drop to 790 boxes per hectare and 1.65 boxes per tree, compared to 1,045 boxes per hectare and 2.22 boxes per tree last season. The average drop rate of oranges is projected to be 17%, slightly higher than previous seasons. This projected increase is mainly due to the increased intensity of citrus greening.

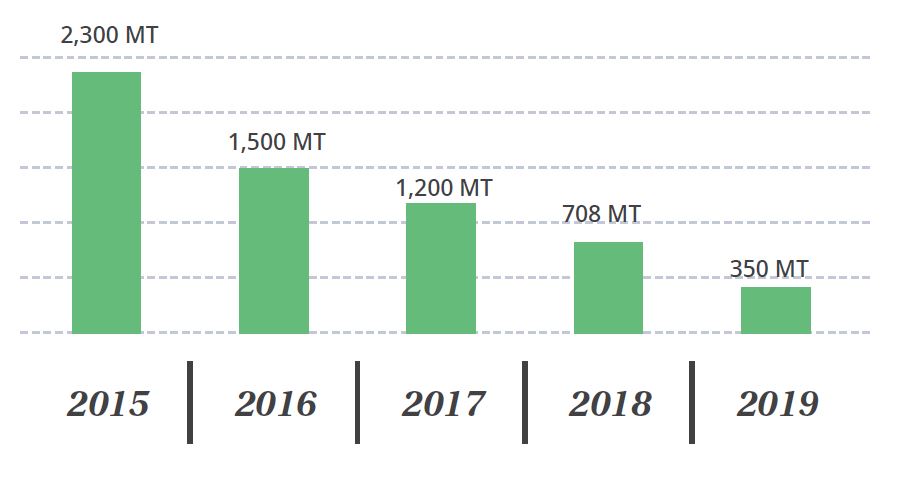

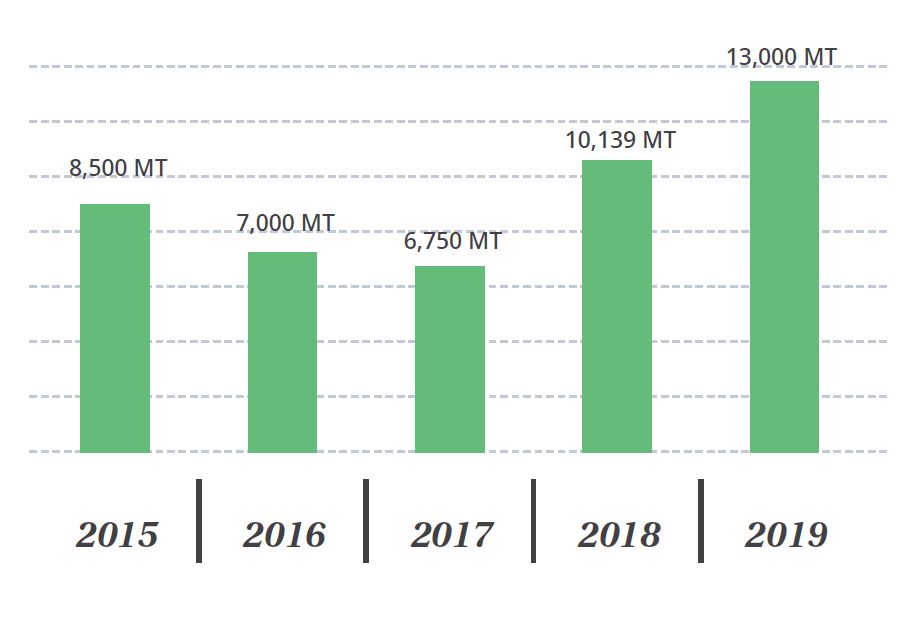

With this reduction in total orange production, fresh fruit consumption is predicted to fall while the amount of oranges for processing is also expected to drop 95 million boxes (3.9 million MT) to 254 million boxes (10.4 million MT). With fewer oranges for processing then production of orange oil, terpenes and juice will decline. Production of CPOO (cold pressed orange oil) is predicted to fall from 42,000 MT in 2019/2020 to 31,000 MT in 2020/2021 while CPOO exports are forecast to rise 31,000 MT to 41,000 MT during the same period, leading to a significant reduction in inventories. Similarly, during the period, d’limonene production is forecast to fall from 34,000 MT to 25,000 MT while d’limonene exports are predicted to fall by a similar amount from 34,000 MT to 24,000 MT. On the positive side, this increase in demand, together with the expected lower crop, is likely to push prices up after the significant decrease in 2019 when the industry experienced record historical low prices for orange oil and terpenes.

In addition, processing may be delayed by two to three months and yields and quality affected by multi-blossoming. Orange juice production is expected to drop 25% to around 24.3 million boxes (992,000 MT). Even though exports of orange juice are forecasted 27% lower, Brazil remains the largest producer and is expected to account for over three-quarters of global exports with slightly higher consumption and stocks.

The outbreak of COVID-19 is generating both positive and negative impacts on the industry with an outcome hard to predict. Global demand for fresh oranges, for example, has increased due to their high content of vitamin C, but has also decreased due to restaurants, schools and food services being closed. Meanwhile labour availability throughout the supply chain is likely to fall as people are affected by the virus and possible lockdown. In addition, there are some reported issues relating to plant maintenance and the availability of spare parts and equipment. At the national level, the volatility of the Brazilian real combined with political instability are adding to the sector’s problems

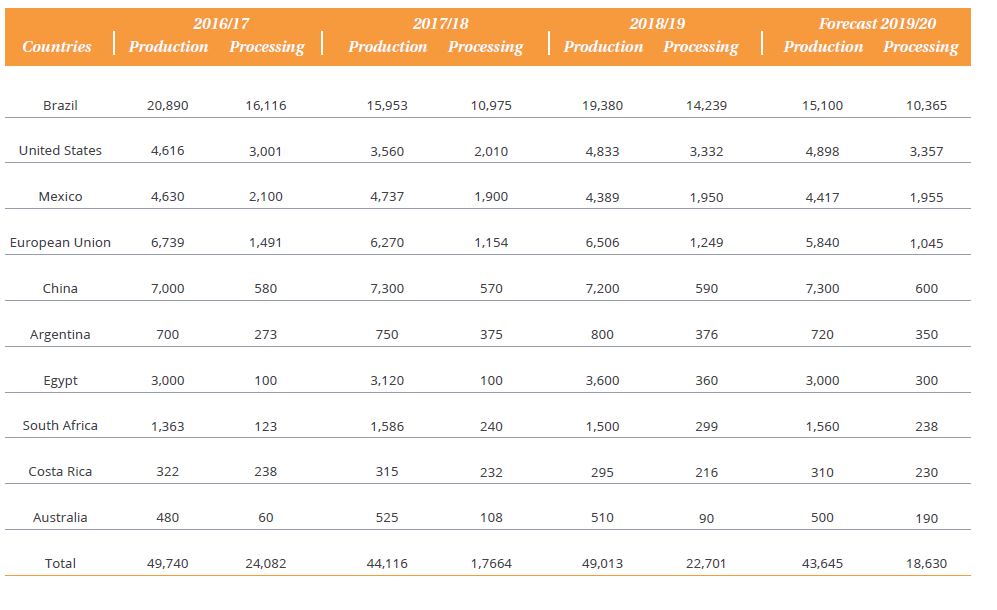

USDA ESTIMATED ORANGE PRODUCTION AND PROCESSING 2016/17 to 2019/20 (million MT)

Market price USD 7.00/kilo

Over 90 products from more than 25 countries analysed and reported on, many with in-depth analysis. The report is also packed with additional articles related to Tackling the COVID-19 crisis: Interview with Ravi Sanganeria, Sustainability Red Alert: Learning the Hard Way, Fanny Bal on Naturals: A New Generation’s Perspective and Nature’s Miracle Mantras: The Australian Power House.

Over 90 products from more than 25 countries analysed and reported on, many with in-depth analysis. The report is also packed with additional articles related to Tackling the COVID-19 crisis: Interview with Ravi Sanganeria, Sustainability Red Alert: Learning the Hard Way, Fanny Bal on Naturals: A New Generation’s Perspective and Nature’s Miracle Mantras: The Australian Power House.