Indonesia – Current & Future Market Dynamics October 14, 2015

Will Indonesia continue to be a major supplier of essential oils, such as cloves, nutmeg, patchouli, citronella, vetiver and other natural ingredients to the global F&F industry? This presentation reviews the challenges and opportunities facing Indonesia’s ingredient supply sector with particular emphasis on Indonesia’s current and future market dynamics.

Indonesia is often in the news for the wrong reasons. You can easily read and hear issues about poverty, pollution, terrible weather, tsunamis, active volcanoes, corruption, man-made disasters and other less than heart-warming stories. However, what is it really like to live and work in Indonesia and what are the possibilities no matter what the challenges may be?

The article takes you through some basic facts about Indonesia and how these facts can be connected to our industry. Then we can focus on the main products our market uses and expects from the region, what may have changed in recent times and what may continue to change in the near future.

Go direct to read about your product of interest – Clove | Patchouli | Nutmeg | Citronella | Vetiver

GEOGRAPHY AND DEMOGRAPHICS

GEOGRAPHY AND DEMOGRAPHICS

First let’s point out where exactly Indonesia is. Well it’s not just one, two or three Islands, but around 18,000, of which over 1,000 are inhabited permanently by Indonesia’s vast 250 MILLION AND INCREASING POPULATION!! That’s a lot people and a lot of islands expanding over AN AREA WIDER THAN NORTH AMERICA! This can create major transport and other logistical problems.

WEATHER

Indonesia lies on the equator, which brings a mixture of heat, humidity and rains, which can be a good recipe for agriculture. Unfortunately, that said, it can also bring about many extremes which can cause both short and long term damage to crops and supply.

We are currently in an El Niño year and Indonesia is one region that can be affected by such global weather patterns more than others. This year’s pattern suggests THE LATEST EL NIÑO EVENT COULD BE THE LARGEST SINCE 1997 and continue until the Spring of 2016 – something that may not only challenge Indonesia but also other countries around the world.

We are currently in an El Niño year and Indonesia is one region that can be affected by such global weather patterns more than others. This year’s pattern suggests THE LATEST EL NIÑO EVENT COULD BE THE LARGEST SINCE 1997 and continue until the Spring of 2016 – something that may not only challenge Indonesia but also other countries around the world.

The last El Nino, which happened five years ago, led to droughts in Australia, blizzards in North America, a heat wave in Brazil and floods in Mexico. It varies with each formation, but it typically brings heavier rain to South America, fewer Atlantic hurricanes, and stronger Pacific typhoons.

The last El Niño also led to drier conditions in Indonesia and the Philippines – a pattern we are already seeing again in parts of Indonesia as we speak and which will impact on some crops in the short term.

FORECASTERS ARE PREDICTING A DRY SPELL UNTIL MARCH 2016

In contrast to this forecast, the region has seen a growing increase in rainfall over recent years, a fact that can contribute to lower yields and shorten harvest periods for most products.

Sadly, climatic changes are not just challenges for us, but the industry as a whole. How we adapt will determine our success.

So already we have touched on two issues we must deal with – logistics and weather, the two of which don’t work well together, which means moving goods from one island to another is already a challenge. Let’s keep that in mind.

ECONOMY AND CURRENCY

Indonesia has the largest economy in South East Asia and with 14.4% of its GDP coming from agriculture this is a very important sector. Because of its proximity to the equator and the existence of over 150 active volcanoes, many Indonesian Islands have rich, fertile soils, perfect for growing a variety of products, making Indonesia one of the world’s most bio-diverse countries. With over 40% of Indonesia’s workforce employed in the agricultural sector, residents have to adapt and think long-term as their livelihood is not just for today but also for many years ahead.

The country has been able to boast GDP GROWTH OVER THE PAST DECADE AT OVER 5% per year and has recently reported a 2% reduction in poverty headcounts since 2010. Back in the Asian Financial crisis of 1998 this was a remarkable 24% of the population! Although GDP growth has slowed in recent years, the recent transition to a new government has raised expectations, with the World Bank predicting good solid GDP growth of 5.5% in 2015 and 6% in 2016.

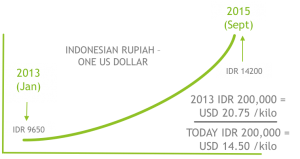

Currency plays a major part in the stability of export pricing for all Indonesian products. Generally, we work on the basic principle that supply and demand are our biggest contributors to what makes ‘today’s market price’, but when you work with a currency that can swing one way or another by 10% in a week, this can bring many complications. In fact, over the past 18 months the Indonesian Rupiah (IDR) value against the US Dollar has weakened significantly from 11,000 IDR to 14,200 IDR – which is over a 20% swing. This not only makes export prices cheaper / more competitive at times but also can mask what is really happening to the supply situation on the ground where local prices for raw materials can be going up or down. Another point to remember.

Currency plays a major part in the stability of export pricing for all Indonesian products. Generally, we work on the basic principle that supply and demand are our biggest contributors to what makes ‘today’s market price’, but when you work with a currency that can swing one way or another by 10% in a week, this can bring many complications. In fact, over the past 18 months the Indonesian Rupiah (IDR) value against the US Dollar has weakened significantly from 11,000 IDR to 14,200 IDR – which is over a 20% swing. This not only makes export prices cheaper / more competitive at times but also can mask what is really happening to the supply situation on the ground where local prices for raw materials can be going up or down. Another point to remember.

It is estimated that the export revenues of essential oils, natural extracts, derivatives and natural isolates have a net income for Indonesia of around $500 million. A sizeable amount!!

The banking system itself is fragile and rarely supports those needing to find finance to improve their cash flow. Interest rates are double digit and the number of reputable lenders is few and far between. This means that many exporters in our market need to have the ability to self-finance, as the crude raw material side of the supply-chain is cash intensive. From the procurement of raw materials when the cash is first exchanged to the receipt of the funds from the client for the final product can take a matter of months rather than weeks and we are not talking about cheap commodities!

ENVIRONMENTAL ISSUES

Since 2009 there has been a 7.5% DECREASE IN FOREST AREAS brought about by illegal logging, forest fires and mining. If this continues at the same rate, by 2050 Indonesia could lose 30% of its forestry land mass and its earning potential.

Rising sea levels will also cause a long-term problem, with some experts saying as many as 1,500 OF INDONESIA’S ISLANDS COULD BE UNDER WATER by the year 2050. Other areas of the mainland, including Jakarta International Airport, the country’s largest airport, which is only 30kms away from Jakarta, are also expected to be under water as early as 2030! .

This could affect up to 40 million people who live within 3 kilometres of Indonesia’s coastlines.

ESSENTIAL OIL PRODUCTION

So how do all these challenges leave our products going forward? What changes have we seen lately and what is likely to come next?

We should note that aside from the obvious global volumes associated with the likes of mint and citrus products in the market, INDONESIA PRODUCES THREE OF THE MOST WIDELY USED NATURAL ESSENTIAL OILS, in terms of volume, natural essential oils in our industry, namely citronella, clove leaf and patchouli – not to mention many others which are highly important, such as nutmeg, vetiver and cajuput to name a few.

| INDONESIAN ESSENTIAL OIL PRODUCTION (2013-2014) | ||||

| Essential Oil | Output 2013 (MT) | Output 2014 (MT) | Trend (2015) | |

| 1 | Clove (Leaf/Stem/Bud) Oil | 3,500 – 4,000 | 3,500 – 4,000 | Stable |

| 2 | Patchouli Oil | 900 – 1,100 | 1,100 – 1,300 | Stable |

| 3 | Nutmeg Oil | 320 -350 | 350 – 400 | Up |

| 4 | Cajeput Oil | 300 – 350 | 300 – 350 | Down |

| 5 | Citronella Oil | 300 – 350 | 350 – 400 | Up |

| 6 | Vetiver | 25 – 30 | 25 – 30 | Down |

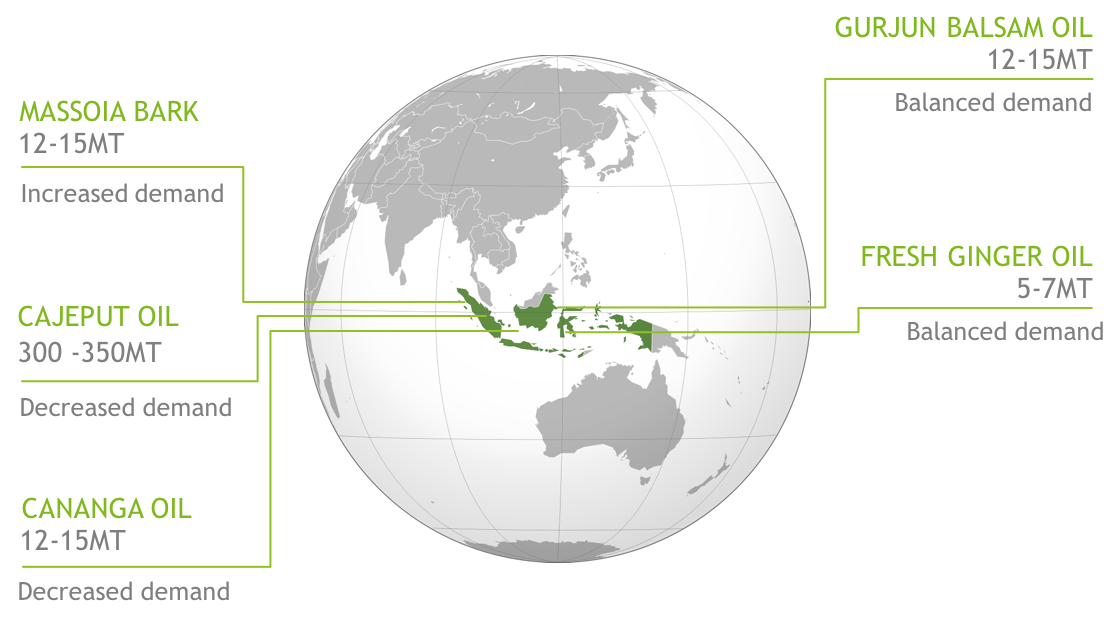

| 7 | Cananga Oil | 12 – 15 | 12 – 15 | Down |

| 8 | Massoia Bark Oil | 12 – 15 | 12 – 15 | Up |

| 9 | Gurjam Balsam Oil | 8 – 10 | 30 – 40 | Stable |

| 10 | Fresh Ginger Oil | 5 – 7 | 5 – 7 | Stable |

CLOVE

Clove is by far the largest essential oil produced in Indonesia based on volume. It is estimated there is in excess of 440,000 HECTARES PRODUCING AROUND 80,000 TONNES OF CLOVE BUDS, predominately in the islands of Java, Sulawesi and Sumatra.

This results in a staggering annual production of around 3,500 – 4,000 tonnes of oil. The primary use of clove is in the domestic clove cigarette industry as well as for flavour and fragrance, which includes Chinese vanillin production, cattle feed and construction.

This results in a staggering annual production of around 3,500 – 4,000 tonnes of oil. The primary use of clove is in the domestic clove cigarette industry as well as for flavour and fragrance, which includes Chinese vanillin production, cattle feed and construction.

Production of clove oil is done by literally hundreds of small traditional distilleries, spread over a large area of Java and South Sulawesi.

A number of clove derivatives are also produced in Indonesia, a product area that is continuing to grow with the introduction of new technologies. Pursuing the value-added route has given Indonesian producers more security in their long-term business model, getting them closer to the end-user.

Whilst clove production can suffer given the longer and heavier rainfall periods, the growing use of cloves in local market applications means that farmers respond to any yield reductions by trying to expand the production area.

Today clove production is stable but should we experience any climatic changes like longer period of rainfall or excessive dry spells we would surely see farmers increasing plantations to compensate, ensuring output remains stable in the future.

As a result, Indonesia will continue to be a leader in the global clove markets.

PATCHOULI

Patchouli is a favourite for many perfumers and is perhaps the most important natural for the fragrance markets. LOCAL VOLUMES REPRESENT AROUND 90% OF GLOBAL PRODUCTION. Depending on the export price it can also represent as much as 35% OF INDONESIA’S TOTAL EXPORT REVENUES from natural essential oils.

The product has undergone something of a revolution in recent years as almost all cultivation has shifted from Java and Sumatra to the islands of Sulawesi. This is not a case of planting near by. As can be seen from the map, some parts of Sulawesi are thousands of kilometres from Sumatra where some exporters are based.

The product has undergone something of a revolution in recent years as almost all cultivation has shifted from Java and Sumatra to the islands of Sulawesi. This is not a case of planting near by. As can be seen from the map, some parts of Sulawesi are thousands of kilometres from Sumatra where some exporters are based.

This MIGRATION has taken place over 10 years at the start of which Java and Sumatra contributed 80% of all raw materials. Today that same figure can be credited to Sulawesi. This is a continuous process as certain components and nutrients in the soil, which the plant needs, are depleted over time. Over a five-year period what was once a good area will become a bad one, so plantations need to be moved to different areas and often to different islands.

With the migration of patchouli to the islands of Sulawesi there has been a quality shift, which is different and somewhat inferior to the previous qualities processed in Java and Sumatra.

Growing conditions in Sulawesi give us three new challenges:

- The high acidic soil results in a much higher acid level in the finished product, which falls well above the industry’s expectations.

- Sulawesi’s flatter lands do not allow water to run off the plantations, as they would need, like they did naturally on other islands.

- This land remained unused for many decades so the soil lacks all the nutrients the plant would like to absorb.

These factors have resulted in longer processing and distillation times, as the material needs to be fractionated and acid washed. It also impacts on the costs and limits production to those who can work with this quality. Processors need to have the correct equipment and have a well-established procurement setup in the Sulawesi region.

The differences in production areas over the past decade are clearly illustrated here when compared to the last visual.

The differences in production areas over the past decade are clearly illustrated here when compared to the last visual.

In the past, people would sit on stocks for months, even years, but now due to fewer and fewer traditional traders and processors in the market place; the maturity of oil currently available is an issue. Patchouli matures with age and this is something that today’s market economics does not allow to happen. Goods are shipped freshly distilled and can be in production in a matter of weeks. This means that some distillers or buyers are having to aerate the material to start the natural maturing process in order to enhance the odour. Carrying 10 tonnes of patchouli in stock can add around $400,000 – $600,000 to an inventory, which is not something most fragrance manufacturers can accommodate. Stock turnover controls like Net Working Capital do not lend themselves favourably to having aged stock, which would ensure your product matures well before use!!

Whether the market likes the new quality or not, it is here to stay. Many end-users have already, or are in the process of, revising their standards to ensure they are able to buy today’s standard quality. The consequences of not addressing these issues can result in companies being restricted to trying to buy a quality that is not readily available.

Some good news has been the recent change in patchouli’s price volatility. History will show dramatic trend curves when it comes to export pricing. The reduction in the number of local exporters combined with more controls at Sulawesi collection points and less speculation has meant steadier prices for the product. What will happen in the future is something unknown to all of us. Market demand sometimes change quickly independently of unseasonal dry or wet weather patterns which can again highlights the lack of stocks available within the supply chain. It can be said that many have enjoyed the benefits of this stability and all buyers, exporters and end-users should continue to work together to ensure this pattern remains in place.

NUTMEG

Nutmeg is a favourite for many, including myself and over the past two decades has been on many rollercoasters! The introduction of new plantation oil in 2014 saw a profound change in the market price of nutmeg. It lost over half of its value in a matter of months!

INDONESIA EXPORTED AROUND 350-400 TONNES OF OIL in both 2013 and 2014, which accounts for around 80% OF GLOBAL PRODUCTION. New plantations began 7-10 years ago after a period of low yielding trees in Aceh created reduced supply and in turn increased prices. This encouraged farmers to plant new trees in other areas of Indonesia such as Java and Sulawesi. (Read more about Indonesia’s Nutmeg plantations here)

INDONESIA EXPORTED AROUND 350-400 TONNES OF OIL in both 2013 and 2014, which accounts for around 80% OF GLOBAL PRODUCTION. New plantations began 7-10 years ago after a period of low yielding trees in Aceh created reduced supply and in turn increased prices. This encouraged farmers to plant new trees in other areas of Indonesia such as Java and Sulawesi. (Read more about Indonesia’s Nutmeg plantations here)

Known as the lazy man’s crop, nutmeg does not need a lot of maintenance and it had been difficult to estimate how many new plantations there may be around North Sulawesi and West Java, where many plantations where established almost simultaneously. This brought an influx of raw materials into the market driving prices down sharply due to over supply.

When this happens the increase in supply inevitably forces prices down but this can be an unhealthy position in both the short and long term. Yes, many end users will enjoy the benefits of lower prices but the reality can be somewhat different. Farmers will be disappointed in their returns and processors will have lost any value-added positions as the prices fall. This is likely to result in fewer collections of raw material at a time when more end-users could be using more product, due to the attractive price, thus potentially causing a future REVERSE IN THE SUPPLY AND DEMAND PATTERNS. It is difficult to predict, but this is one sustainability project that could backfire or maybe it will reignite some lost interest in this once popular spice? Time will tell but which ever it is, we are confidant Indonesia will remain the largest global producer for many years to come.

CITRONELLA

CITRONELLA

Citronella is the one we know as the ‘bug killer’. Indonesia has re-emerged as a strong producer of this product after many years in the shadows of China’s production. However, this time it is not because of any ingenious plan or changes in crop conditions. In fact, most of Indonesia’s citronella production is consumed internally and the production figures have not change by much. So why has Indonesia’s competitiveness changed for the better in the international market?

This time perhaps the BIGGEST CONTRIBUTOR HAS BEEN THE CHANGE IN EXCHANGE RATES. The 15-20% difference we mentioned earlier in the Rupiah’s weakness against the US Dollar has made export prices more competitive. The slide provides a comparative example of how big the difference can be when local prices remain the same.

On a more positive and sustainable note, some NEWER PLANTATIONS IN SUMATRA AND OTHER PARTS OF JAVA HAVE BEEN INTRODUCED and we do expect supplies to get better in the near future. This should ensure there is surplus product available from the domestic market to keep supplies heading into the global arena. However, it could also be short-lived should the currency work against Indonesian exports anytime in the near future.

On a more positive and sustainable note, some NEWER PLANTATIONS IN SUMATRA AND OTHER PARTS OF JAVA HAVE BEEN INTRODUCED and we do expect supplies to get better in the near future. This should ensure there is surplus product available from the domestic market to keep supplies heading into the global arena. However, it could also be short-lived should the currency work against Indonesian exports anytime in the near future.

There is no doubt citronella will feature in Indonesia’s future output, but most of that confidence relates to its domestic market. As for exports, much will depend on the currency and China’s approach to losing some market share.

VETIVER

The dynamics of this product have changed dramatically over the past year. For years this was a fairly dormant product with very little interest shown by the global market. However, due to reduced availability from other producing countries, particularly Haiti, and an increase in usage, the interest in Indonesian vetiver has increased over the past couple of years. This in turn has added additional pressure on supply.

The dynamics of this product have changed dramatically over the past year. For years this was a fairly dormant product with very little interest shown by the global market. However, due to reduced availability from other producing countries, particularly Haiti, and an increase in usage, the interest in Indonesian vetiver has increased over the past couple of years. This in turn has added additional pressure on supply.

Yields from the distillation of vetiver are suffering; declining since 2011, mainly due to the prolonged rainy seasons we keep mentioning. Additionally, costs such as LABOUR AND FUEL HAVE BEEN MOVING UP ANNUALLY BY AN AVERAGE OF 15-20%, adding to production costs. As prices of vetiver have seen no real increase in previous years local farmers have been discouraged from investing in new plantations.

As demand increased, prices started moving up in February 2015 and jumped again suddenly around April 2015 to levels of 2.2 million rupiah per kg – 2½ TIMES HIGHER THAN ONLY 12 MONTHS AGO! This price movement has started to encourage farmers to return to the product but very slowly, suggesting that prices may rise further or at least not reduce until either demand falls or supplies increase.

As demand increased, prices started moving up in February 2015 and jumped again suddenly around April 2015 to levels of 2.2 million rupiah per kg – 2½ TIMES HIGHER THAN ONLY 12 MONTHS AGO! This price movement has started to encourage farmers to return to the product but very slowly, suggesting that prices may rise further or at least not reduce until either demand falls or supplies increase.

There is little doubt the industry is looking for solutions to find a sustainable supply of vetiver. Whether Indonesia can provide these solutions remains unknown for the immediate future.

OTHER INDONESIAN NATURALS

OTHER INDONESIAN NATURALS

The list of other Indonesian naturals could be endless! In the slide a number of other important naturals that play an active role in the industry are mentioned. Each has its own sets of dynamics, which can change over time just like the others mentioned.

In general, the demand for essential oils, natural derivatives and isolates is growing.

The Indonesian people are very excited and passionate about having more technology and information available in order to create new products, which will be introduced into the industry over time. We have already seen many examples of the industry coming closer to the farmers to create new naturals and partnerships which will ensure Indonesia becomes a strong partner for many years to come.

MORE OILS INCLUDE SANDALWOOD, KAFFIR LIME, CUBEB, BLACK PEPPER, AGARWOOD & MANY NEW NATURAL ISOLATES

CONCLUSIONS

In conclusion, how can we best summarise the climate changes, the infrastructure issues and the economic revolutions on one side of the coin, then on the other side the efforts to create new plantations, the expansion in the number of local producers and the attempts to stabilise the market?

The simple way would be to say it is Indonesia. The challenges will always exist – let’s not fool ourselves into saying we can change the world quickly with new co-operatives, plantations, joint ventures and other initiatives. We, like others, will try to do this and, like others, we all agree that we have to start somewhere. However, the fact remains this is a challenging place to do business but a challenge we must face, as Indonesia is critically important in creating some great products that our industry certainly cannot live without.

One significant step the Indonesian essential oil industry must do is to ensure that farmers of all the different products gain fairly from their hard work. This is something the industry as a whole has to come together to achieve with real sustainable solutions. Today we hear talk of this but the sad reality is that many projects are simple PR exercises looking to tick the box on social-economic responsibility. We need a system that is accredited and judged fairly so those intended beneficiaries of any project are the ones who actually benefit. This must start today!

So we will continue to accept the challenges in the right spirit and in return I’m sure Indonesia, with a little encouragement, will keep providing us with what we need. Good quality, innovative and competitive natural essential oils.

Paper presented by Ravi Sanganeria at IFEAT Sri Lanka Conference September 27 – October 1, 2015 on behalf of Ultra International B.V. and P.T. Van Aroma