NATURALS FROM INDONESIA – AN UPDATE January 27, 2022

Ravi Sanganeria

At the last IFEAT Conference in Bali in October 2019 I made a keynote presentation providing an overview of Indonesian essential oils and the many challenges and opportunities faced by the sector. Since then, the past two years have probably been the most difficult faced by the sector in living memory and this article provides an update of some recent key developments.

TRENDS IN THE PRODUCTION OF MAJOR INDONESIAN ESSENTIAL OILS

Indonesia continues to be a dominant and diverse supplier of natural ingredients to the world’s F&F industry exporting at least 40 essential oils. It is the major global supplier of patchouli, cloves, nutmeg, and vetiver. This section reviews some key features and trends of these major oils as well as citronella, vetiver, and vanilla. Of course, Indonesia provides many other essential oils to our industry. These include cananga, cajeput, cinnamon, cubeb, fennel, ginger, gurjun balsam, kaffir lime, lemongrass, massoia, black pepper, sandalwood, and agarwood – but these are not discussed although the table provides estimates of Indonesian output of these items.

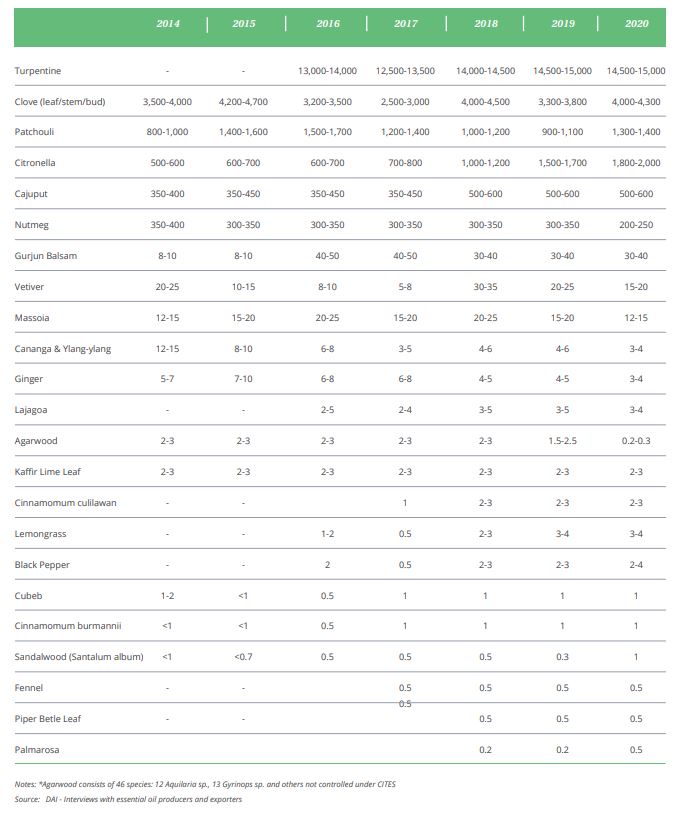

INDONESIA: ESTIMATED ESSENTIAL OIL PRODUCTION 2014 -2020 (METRIC TONNES)

Indonesian essential oil production activities are spread throughout a very large country and involve many parties in the value chain ranging from predominantly smallholder farmers producing raw materials, to an estimated 3,300 small and medium-sized distilling operations, collectors, and traders, to technically advanced processing industries and exporters. Essential oils provide work and income for many of Indonesia’s rural communities, often in remote areas, and are of great importance to the economic, social, and environmental wellbeing of an estimated 200,000 people in these communities. In addition, the sector is continuing to produce more value added products, such as CO2 extracts.

Citronella (Cymbopogon winterianus Jowitt)

Citronella is a perennial grass grown by smallholders that is relatively easy to cultivate. It can be hand-harvested every three months and distilled throughout the year, using basic equipment and techniques. No additional fertiliser and weeding are required and it acts as a natural pesticide. Recently Indonesian production has grown very quickly with the opening of new planting areas and annual output is estimated at 1,800-2,000 MT. Production has been moving eastwards particularly in Java and into Sulawesi. As production expands there is also a lot of out-of-specification material available in the market. Because of substantial local consumption, only 300-350 MT is exported. Indonesia has recently overtaken China as the world’s largest citronella oil producer. Indonesian citronella is better priced than citronella from China, Vietnam, and Sri Lanka but price volatility is considerable.

Citronella is a perennial grass grown by smallholders that is relatively easy to cultivate. It can be hand-harvested every three months and distilled throughout the year, using basic equipment and techniques. No additional fertiliser and weeding are required and it acts as a natural pesticide. Recently Indonesian production has grown very quickly with the opening of new planting areas and annual output is estimated at 1,800-2,000 MT. Production has been moving eastwards particularly in Java and into Sulawesi. As production expands there is also a lot of out-of-specification material available in the market. Because of substantial local consumption, only 300-350 MT is exported. Indonesia has recently overtaken China as the world’s largest citronella oil producer. Indonesian citronella is better priced than citronella from China, Vietnam, and Sri Lanka but price volatility is considerable.

Consumption has been growing, reflecting its wide range of uses. These include use in cosmetics, perfumery, aromatherapy, insect repellents, various medicinal purposes, and potential use in biofuel. Although citronella oil is produced organically it is not currently certified.

Cloves (Eugenia caryophyllata, syn. Syzygium aromaticum)

Indonesia is the world’s biggest producer and consumer of cloves, producing an estimated 80,000 MT each year from some 440,000 hectares located mainly in Sulawesi (accounting for 60% of clove production), Java and Sumatra. Most clove buds are used domestically in the “kretek” cigarette industry. Clove oil is produced from the clove buds, leaves and stems and clove oils are the second largest essential oil produced in Indonesia, after turpentine oil. Annual oil production has shown wide fluctuations with 2020 annual output estimated at 4,000 – 4,300 MT although production dipped to between 3,300 and 3,800 MT in 2019. Climatic factors are an important factor behind the annual fluctuation and every fourth year Indonesia tends to have a large harvest lasting 3 – 4 months. Unseasonal weather patterns including excess rain have affected the availability and increased supply uncertainties. Despite variations in annual output and prices, current estimates suggest that the overall production trend is stable. Clove oil production is done by hundreds of small traditional distilleries, spread over large areas of Java, Sumatra, and Sulawesi. All the major clove oil distillers are concentrated in Java, close to the kretek cigarette factories. Within Indonesia, sizeable investments are being made to produce value added clove products. Such investments provide clove producers with greater security. There is a strong demand for clove derivatives, in part because of new applications (e.g., in animal feed and pheromones).

Indonesia is the world’s biggest producer and consumer of cloves, producing an estimated 80,000 MT each year from some 440,000 hectares located mainly in Sulawesi (accounting for 60% of clove production), Java and Sumatra. Most clove buds are used domestically in the “kretek” cigarette industry. Clove oil is produced from the clove buds, leaves and stems and clove oils are the second largest essential oil produced in Indonesia, after turpentine oil. Annual oil production has shown wide fluctuations with 2020 annual output estimated at 4,000 – 4,300 MT although production dipped to between 3,300 and 3,800 MT in 2019. Climatic factors are an important factor behind the annual fluctuation and every fourth year Indonesia tends to have a large harvest lasting 3 – 4 months. Unseasonal weather patterns including excess rain have affected the availability and increased supply uncertainties. Despite variations in annual output and prices, current estimates suggest that the overall production trend is stable. Clove oil production is done by hundreds of small traditional distilleries, spread over large areas of Java, Sumatra, and Sulawesi. All the major clove oil distillers are concentrated in Java, close to the kretek cigarette factories. Within Indonesia, sizeable investments are being made to produce value added clove products. Such investments provide clove producers with greater security. There is a strong demand for clove derivatives, in part because of new applications (e.g., in animal feed and pheromones).

Nutmeg (Myristica fragrans Houtt.)

Indonesia dominates world production of nutmeg and nutmeg oil, accounting for approximately 80% of global output. Annual Indonesian nutmeg oil production in recent years has averaged between 300 – 350 MT, although 2020 production fell to an estimated 200 – 250 MT. Unlike some crops, such as patchouli and vanilla, which are very labour intensive, once nutmeg has been planted it is relatively easy to maintain and harvest. Moreover, farming and distillation methods for nutmeg oil are more organised and concentrated than other Indonesian essential oils.

Indonesia dominates world production of nutmeg and nutmeg oil, accounting for approximately 80% of global output. Annual Indonesian nutmeg oil production in recent years has averaged between 300 – 350 MT, although 2020 production fell to an estimated 200 – 250 MT. Unlike some crops, such as patchouli and vanilla, which are very labour intensive, once nutmeg has been planted it is relatively easy to maintain and harvest. Moreover, farming and distillation methods for nutmeg oil are more organised and concentrated than other Indonesian essential oils.

Patchouli (Pogostemon cablin)

Patchouli oil is one of the most sought-after ingredients for fine fragrances and Indonesia d ominates global production, with annual exports of 1,200 – 1,500 MT accounting for approximately 90% of international trade. Considerable efforts are being made to improve sustainability and stabilise production and prices but for a variety of reasons including the impact of climatic factors (drought in 2019, heavy rains, El Niño), pests and disease, shifting cultivation, the fluctuations and volatility of the process has continued. In late 2021 the unseasonal weather patterns and heavy rain severely impacted the availability, quality, and prices of patchouli. Sulawesi produces over 1,000 MT and now accounts for some two-thirds of Indonesia’s patchouli oil output. Despite efforts to stabilise the supply sources there is evidence of a continuing shift of the crop from southeast Sulawesi to central and north Sulawesi creating a more cumbersome supply chain and greater price volatility.

ominates global production, with annual exports of 1,200 – 1,500 MT accounting for approximately 90% of international trade. Considerable efforts are being made to improve sustainability and stabilise production and prices but for a variety of reasons including the impact of climatic factors (drought in 2019, heavy rains, El Niño), pests and disease, shifting cultivation, the fluctuations and volatility of the process has continued. In late 2021 the unseasonal weather patterns and heavy rain severely impacted the availability, quality, and prices of patchouli. Sulawesi produces over 1,000 MT and now accounts for some two-thirds of Indonesia’s patchouli oil output. Despite efforts to stabilise the supply sources there is evidence of a continuing shift of the crop from southeast Sulawesi to central and north Sulawesi creating a more cumbersome supply chain and greater price volatility.

Turpentine (Pinus merkusii)

Turpentine is a renewable product extracted from pine trees (Sumatran pine), produced as a by-product from tapping trees for resin or from cellulose pulp production. Production has been growing and is between 14,000 – 15,000 MT and is a very labour-intensive industry. Unlike most Indonesian essential oils, turpentine is produced predominantly on government-owned estates in Java and Sumatra. Most of the turpentine derivatives used in F&F are chemically transformed and therefore considered synthetic by regulatory bodies. Turpentine derivatives, particularly terpenes are a vital source of F&F ingredients, particularly for use in fragrances and the industry is looking towards these derivatives as a vital source of renewable feedstocks in the future.

Turpentine is a renewable product extracted from pine trees (Sumatran pine), produced as a by-product from tapping trees for resin or from cellulose pulp production. Production has been growing and is between 14,000 – 15,000 MT and is a very labour-intensive industry. Unlike most Indonesian essential oils, turpentine is produced predominantly on government-owned estates in Java and Sumatra. Most of the turpentine derivatives used in F&F are chemically transformed and therefore considered synthetic by regulatory bodies. Turpentine derivatives, particularly terpenes are a vital source of F&F ingredients, particularly for use in fragrances and the industry is looking towards these derivatives as a vital source of renewable feedstocks in the future.

Vanilla (V. planifolia and V. tahitensis)

Indonesia is the world’s third largest producer of natural vanilla, after Madagascar and Papua New Guinea. Annual output is difficult to estimate in part because of sizeable imports from neighbouring PNG. Recent Indonesian output has been estimated at 100 to 150 MT compared with approximately 300 MT in PNG. The high prices of recent years have led to an expansion of Indonesian planting which in turn should lead to a rise in production.

Indonesia is the world’s third largest producer of natural vanilla, after Madagascar and Papua New Guinea. Annual output is difficult to estimate in part because of sizeable imports from neighbouring PNG. Recent Indonesian output has been estimated at 100 to 150 MT compared with approximately 300 MT in PNG. The high prices of recent years have led to an expansion of Indonesian planting which in turn should lead to a rise in production.

The vanilla sector faces several challenges, which include natural disasters in some growing areas (e.g., landslides, tropical cyclone), higher freight cost and less frequency of shipment activities due to the Covid-19 pandemic, and high prices leading to early harvesting practices.

Vetiver (Vetiveria zizanioides).

Demand for vetiver has been growing, encouraged by greater use in aromatherapy. Value added products are being produced (e.g., vetiver CO2 extract, with a superior olfactory profile, and vetiveryl acetate) helping to raise demand. Increasing interest combined with rising prices encouraged efforts to expand production. Severe precipitation has led to yield variations. Industry is looking for sustainable quality supplies, but whether Indonesia can provide a long-term solution remains to be seen. Indonesian producers have faced criticism for delivering inferior quality but recent developments to enhance quality and improve distillation equipment and processes are leading to improved export quality. Indonesian vetiver oil maintains its unique characteristics and is perceived as a quality product compared to the Haitian material.

Demand for vetiver has been growing, encouraged by greater use in aromatherapy. Value added products are being produced (e.g., vetiver CO2 extract, with a superior olfactory profile, and vetiveryl acetate) helping to raise demand. Increasing interest combined with rising prices encouraged efforts to expand production. Severe precipitation has led to yield variations. Industry is looking for sustainable quality supplies, but whether Indonesia can provide a long-term solution remains to be seen. Indonesian producers have faced criticism for delivering inferior quality but recent developments to enhance quality and improve distillation equipment and processes are leading to improved export quality. Indonesian vetiver oil maintains its unique characteristics and is perceived as a quality product compared to the Haitian material.

THE IMPACT OF THE COVID-19 PANDEMIC

Indonesia has suffered one of the worst COVID-19 pandemic outbreaks in Asia and the world. COVID-19 was confirmed in Indonesia in March 2020 and a month later the virus had spread to all 34 provinces. By early December 2021 some 4.3 million cases had been confirmed and official deaths totalled 144,000, ranking second in Asia and eighth in the world. However, actual figures are likely to be much higher. Unlike many countries, Indonesia did not implement a national lockdown but rather imposed “large-scale social restrictions” (PSBB) later modified to community activity restrictions. Nevertheless, COVID-19 is having an enormous social and human impact in terms of the deaths, illness and numerous disruptions and tragedies it has caused.

The COVID pandemic is having a considerable impact on Indonesia’s economy, and the essential oils sector has not escaped. COVID created four major challenges – logistics, labour, finance, and price volatility. The logistics issue is discussed in a separate section on transport and freight. Labour movement and availability was restricted, thus reducing production capacity and the time required to fulfil supply requirements. Financial issues arose, sometimes operations had to be closed creating difficulties in rotating capital, sometimes raw materials couldn’t be obtained or wages paid. Economic growth either stagnated or declined and there was severe disruption to the supply chain. The F&F secto was less disrupted than many since it was often designated an essential industry.

The COVID pandemic is having a considerable impact on Indonesia’s economy, and the essential oils sector has not escaped. COVID created four major challenges – logistics, labour, finance, and price volatility. The logistics issue is discussed in a separate section on transport and freight. Labour movement and availability was restricted, thus reducing production capacity and the time required to fulfil supply requirements. Financial issues arose, sometimes operations had to be closed creating difficulties in rotating capital, sometimes raw materials couldn’t be obtained or wages paid. Economic growth either stagnated or declined and there was severe disruption to the supply chain. The F&F secto was less disrupted than many since it was often designated an essential industry.

Price fluctuations vary from product to product but were invariably substantial due to demand-supply imbalances. COVID-19 led to one of the most severe global recessions in living memory and although Indonesia experienced a milder recession than many, it was not spared. Following real GDP growth in 2019 of 5% the economy declined by 2.1% in 2020 and almost 3 million people fell into poverty. In 2021 Southeast Asia’s largest economy returned to growth, but growth in the third quarter (July – September) slowed more than expected to an estimated 3.5% (compared with 7% expansion in April – June quarter) as further restrictions to control the deadly Delta COVID-19 variant put a further brake on activity. It was predicted that growth would be getting back on track in late 2021 but this again could be limited by concerns over the new Omicron variant and concerns over trends in the global economy. Uncertainty remains very high with sizeable downside risks.

Unfortunately, in late 2021 the anticipated return to a much greater degree of normality has not materialized as the disruptions due to the COVID-19 pandemic have not subsided. Significant volatility throughout the world continues to plague the ability to operate normally. Supply chain and logistic disruptions continue, demand for many F&F products remains high, while raw material availability is either reduced or uncertain and costs are rising creating many difficulties; labour costs are rising, and severe shipping and freight constraints remain, leading to increased delivery times.

CLIMATE CHANGE

While global climate change is impacting the economies of all countries, the impact on Indonesia is greater than most. There is ample evidence showing that the Indonesian climate is changing. Over the past two decades rainfall patterns have changed with increasing frequency of droughts and floods triggered by the Australasia monsoon and by the El Niño Southern Oscillation (ENSO). Not only are average temperatures rising but also rainfall patterns are changing with the rainy season ending earlier and the length of the rainy season becoming shorter. All economic sectors are affected by the erratic weather patterns but the agricultural sector and output are particularly impacted. This is having negative consequences for rural incomes, food prices, and food security, and a disproportionate impact on the poor.

While global climate change is impacting the economies of all countries, the impact on Indonesia is greater than most. There is ample evidence showing that the Indonesian climate is changing. Over the past two decades rainfall patterns have changed with increasing frequency of droughts and floods triggered by the Australasia monsoon and by the El Niño Southern Oscillation (ENSO). Not only are average temperatures rising but also rainfall patterns are changing with the rainy season ending earlier and the length of the rainy season becoming shorter. All economic sectors are affected by the erratic weather patterns but the agricultural sector and output are particularly impacted. This is having negative consequences for rural incomes, food prices, and food security, and a disproportionate impact on the poor.

A major threat from climate change is the rise in sea levels. Indonesia has an estimated 95,180 km of coastline and coastal areas contain vast areas of agricultural land and account for at least a quarter of national gross domestic product (GDP). Some areas such as Sulawesi are particularly vulnerable. Towards the end of the dry season in September 2021, Sulawesi experienced unseasonal weather patterns with almost non-stop rainfall leading to numerous issues in the region regarding severe flooding, land erosion, crop damage, destruction of infrastructure including roads, bridges, and distillation equipment. The patchouli and clove crops were particularly impacted since the shorter dry season reduced the ability to build up raw material supplies.

Climate change will continue to have a significant impact on agricultural production including essential oil crops. The UN’s Intergovernmental Panel on Climate Change (IPCC) latest report expects year-on-year monsoon rainfall to increase as weather patterns become less predictable. The impact will be both direct (e.g., lower agricultural productivity due to increased air temperature and changes in rainfall patterns, and infrastructure damage) and indirect (e.g., changes in irrigation water availability because of changes in crop evaporative demands and runoff, as well as shifts in the types of pests and diseases affecting crops).

Enhanced awareness by government agencies and companies along the value chain, including farmers, is helping the rural economy adapt to the adverse impacts of climate change. However, much will depend on national policies relating to Indonesia’s forestry and energy (especially coal and oil) sectors, which are not only the two leading sources of livelihoods in Indonesia, but also the country’s top two carbon emitters. The Indonesian Government and many of its institutions are very aware of the impact of climate change on the economy and took a leading role at the recent COP 26 Glasgow climate change discussions. This role will continue in 2022, when Indonesia holds the G20 presidency, and in 2023 when it chairs ASEAN. Substantial commitments were made in Glasgow to substantially reduce Indonesia’s carbon emissions but the implementation of commitments remains a major issue.

LOGISTICS AND TRANSPORT

COVID-19 has created turmoil throughout much of the global transportation systems and Asia has been particularly affected. Asian ports have been closed, lockdowns and the need for testing have restricted labour availability and freight movements; export and import procedures have become more complicated; freighters have been unable to enter ports. Once lockdowns eased, transportation systems have been unable to meet the resurgent demand, leading to the inevitable upward pressure on freight costs and further delays.

COVID-19 has created turmoil throughout much of the global transportation systems and Asia has been particularly affected. Asian ports have been closed, lockdowns and the need for testing have restricted labour availability and freight movements; export and import procedures have become more complicated; freighters have been unable to enter ports. Once lockdowns eased, transportation systems have been unable to meet the resurgent demand, leading to the inevitable upward pressure on freight costs and further delays.

The worldwide supply chain crisis impacted Indonesia dramatically by pushing up air and sea freight costs several fold and by doubling or even tripling lead times for shipping. Thus, it can take almost six months to ship goods from Asia to the USA or the EU compared with two months pre-COVID. Transportation of some essential oils has not been helped by their classification as “hazardous goods” and a reluctance by some shippers to handle them. Certainly, logistics and transport were one of the most important and severely affected sectors in the COVID-19 pandemic. The movement of ships and aircraft and their cargo was severely restricted and fewer ships and aircraft arrived and departed from Indonesia. Large numbers of containers ended up being in the wrong location and often being unable to be landed and emptied. This increased freight costs, transportation times and reduced shipment volumes. Thus, major obstacles were created along the supply chain and there has been continued uncertainty over procuring space and containers for shipping products and their eventual arrival at export destinations. The proportion of freight costs in the final value of the product has surged.

SUSTAINABILITY, TRACEABILITY AND THE DAI

Globally there is a growing demand for essential oils as consumers increasingly try to move away from synthetic ingredients often obtained from petrochemical sources to “natural” products. A related movement during the past few years has been the pressure, predominantly from consumers and consumer goods companies, for product traceability and the adoption of sustainable agricultural and environmental practices. This has put greater pressure on growers, especially small-scale farmers, who are probably the weakest link in the value chain. Many are operating at or near the poverty line and find it difficult to absorb the additional costs imposed by trying to meet the traceability and sustainability requirements of those along the value chain, particularly the F&F houses. To enable growers to invest in the new practices required several things need to happen:

Globally there is a growing demand for essential oils as consumers increasingly try to move away from synthetic ingredients often obtained from petrochemical sources to “natural” products. A related movement during the past few years has been the pressure, predominantly from consumers and consumer goods companies, for product traceability and the adoption of sustainable agricultural and environmental practices. This has put greater pressure on growers, especially small-scale farmers, who are probably the weakest link in the value chain. Many are operating at or near the poverty line and find it difficult to absorb the additional costs imposed by trying to meet the traceability and sustainability requirements of those along the value chain, particularly the F&F houses. To enable growers to invest in the new practices required several things need to happen:

- Growers need to be supported educationally, technically, and financially

- Consumers and consumer goods companies need to be educated that a price premium must be paid to meet these higher standards

- Local associations can play an important role in this.

In my Bali 2019 presentation I outlined some of the growing range of sustainability initiatives being undertaken in the Indonesian naturals sector, particularly in patchouli and cloves, by local Indonesian companies, major F&F houses, and local organisations. Where possible these initiatives have continued and expanded during the past two years, but they only scratch the tip of the iceberg.

More integrated policy options are needed, including changes in the institutional infrastructure and enhanced stakeholder awareness to adapt not only to the sustainability and traceability demands of consumers but also to the related adverse climate change impacts. A key area is the continued development of sustainable policies based on the three pillars of economic, social, and environmental sustainability. While such policies are now being adopted and implemented in the essential oil supply chain much more needs to be done.

Over the past decade the DAI (Dewan Atsiri Indonesia – Indonesia Essential Oils Council), under the recent chairmanship of Robbie J Gunawan of Indessso, has become an increasingly important force in developing the Indonesian essential oils sector. Its various programmes are encouraging the sustainable growth of the sector by helping empower and train stakeholders, especially smallholders, by supporting and disseminating applied research, by supporting certification schemes and value-added projects.

SOME CONCLUDING COMMENTS

The past two years have seen dramatic global changes that have impacted the way we conduct our business and this will continue for the foreseeable future. In order to survive all the stakeholders in the value chain have had to demonstrate greater adaptability and resilience. The COVID-19 pandemic has increased levels of uncertainty in all aspects of our sector whether it relates to shifting crop patterns, climate change, logistics, labour availability, rising costs, sustainability and changing demand patterns. As one of the major suppliers of natural ingredients to the F&F sector, Indonesia has been at the centre of some of these changes. However, some things have not changed:

- Indonesia continues to be a fascinating country that offers immense opportunities. It is the 10th largest economy in the world and the largest in Southeast Asia, the world’s fourth most populous nation and, until the recent pandemic, had made enormous gains in poverty reduction.

- It can become of even greater importance to the F&F industry in several respects:

- -As a continued major supplier of raw material ingredients

- -As an increasingly important supplier of value-added products

- -As a major market for F&F products

- -And as a leader in agricultural practices and sustainable production of essential oils.